The Anatomy of an HSA [Infographic]

If you are enrolled in a High Deductible Health Plan (HDHP), then you are eligible for a Health Savings Account (HSA). HSAs are an excellent way to save for health care and retirements, as well as pay for current and future eligible medical expenses.

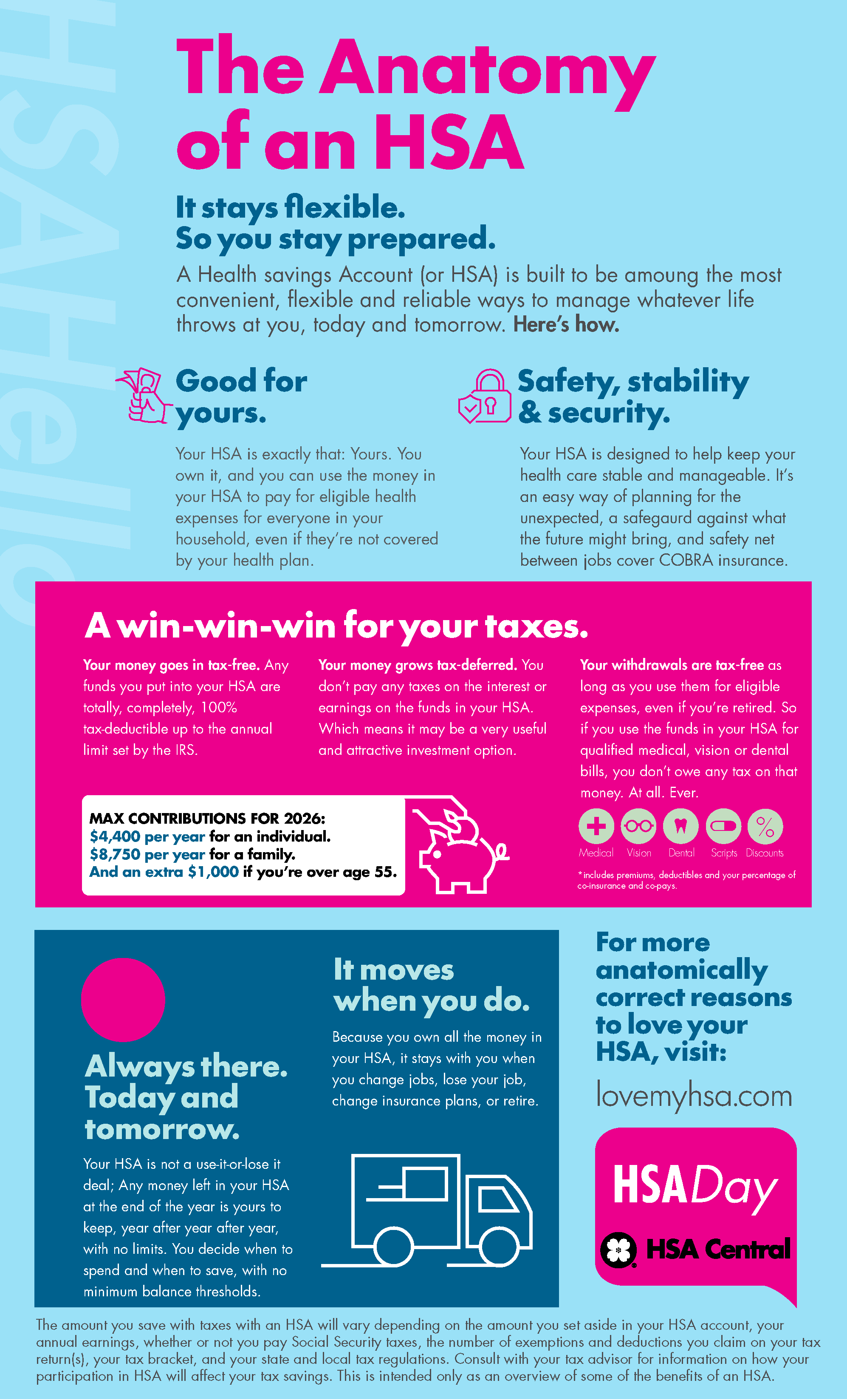

In 2003, HSAs were established by federal law and designed as a financial account to help you save for future healthcare expenses. There are many benefits to both employers and consumers who utilize HSAs to manage healthcare spending and saving, including several tax advantages, which is often referred to as a “triple tax advantage”.

So what exactly is an HSA? Let’s break it down for you.

HSAs provide safety, stability, and security.

HSAs were designed with you in mind, allowing you take control of your healthcare spending and savings by gaining access to your funds when and where you need them. You are able to save money for health-related costs, which can help you plan for the expected and sometimes unexpected life events happening now and in your future. This can even include planning for retirement. HSAs come with the same tax advantages as a 401(k), giving you the ability to withdraw funds for eligible medical expenses without paying taxes.

When you change jobs, your HSA funds go with you.

Accepting a new job can come with the worry of new health insurance and plans. However, the funds in your HSA are all owned by you, and you take those funds with you should you change jobs, lose your job, change insurance plans, or even retire.

HSAs can be used for personal expenses or for family members.

All of the funds in your HSA are owned by you. That means you can use them as you need to for eligible health expenses, which includes doctors’ visits, prescriptions and contacts, and even orthodontics and dentist visits. You can even use your HSA for medical items outside of the doctor’s office like bandages, sunscreen, and dentures. One key benefit of an HSA is that you can also use your funds for eligible health expenses for others in your household, even if they’re not covered by your health plan.

Your HSA funds have a triple-tax advantage.

HSAs were created with the triple-tax advantage, which means your contributions are 100% tax-deductible up to the annual limit set by the IRS. You won’t pay taxes on the interest or earnings on the funds in your HSA, and your withdrawals are tax-free as long as they are used for eligible medical expenses. If you have questions, please consult your tax advisor.

Your HSA funds roll over from year to year.

With flexible spending accounts (FSAs) you’re required to spend a specific amount on medical-related items within a calendar year. HSAs continuously build your savings, year after year. If you don’t use all of your savings in one calendar year, then your HSA simply continues to grow. At the end of the year, there is no rush to submit claims for reimbursement in the fear of losing money.

It’s always important to weigh your options and consider your current healthcare needs when choosing the right healthcare plan for you and your family. Now may be the right time to make the switch to an HSA. Check out our HSA Health Plan Comparison Calculator to see what you could save annually compared to a traditional health plan.